Guidance Papers | GP-2: Preparation for Actual Income Loss (AIL) Claims

Download

Click here for a PDF version (Size: 265 KB - updated: 2008-12-30)

GP-2: Preparation for actual income loss (AIL) claims

- General Principles

- The IAP is a national program. Further, the parties to the Settlement Agreement have signaled an intention to reject differential levels of compensation depending on province of residence by moving from the ADR grid to the national compensation grid. Therefore, for the purposes of determining AIL, national general population data should be used as to such matters as income levels, retirement age, unemployment rates and life expectancy.

- There is general recognition by the parties to the Settlement Agreement that claims for loss of traditional income (whether for consequential loss of opportunity or AIL) are recognized under IAP, providing an appropriate evidentiary foundation is supplied.

- In cases involving AIL, the “plausible link” test does not apply. Adjudicators are instructed to apply the more stringent causation standards applied by the courts, in cases such as Athey, Blackwater, H.L and others.

- The IAP provides that persons with AIL claims that may exceed the $250,000.00 maximum available under IAP, may apply to the Chief Adjudicator for access to the courts.

- AIL should be contrasted against “consequential loss of opportunity,” which, provided the claim is brought within IAP, can be established on the more relaxed standard of “plausible link.” However, the IAP provides (page 8), that claimants may also apply to the Chief Adjudicator for access to the courts, even in claims for consequential loss of opportunity that may exceed the maximum permitted under the IAP grid.

- Canada has agreed that where a claim for AIL is not proven, the claim for loss of opportunity may still be considered under the standard track, applying the “plausible link” test. However, before applying for AIL, claimants and legal counsel are strongly encouraged to carefully consider whether a claimant’s interests are best served:

- In the standard track, where both harms and consequential loss of opportunity are available under the compensation grid based on the more relaxed “plausible link” standard; OR

- In the complex track, where AIL is available, but where both harms and AIL must be established on the higher causation standards established by the courts. AIL is available instead of, not in addition to, consequential loss of opportunity.

- Adjudicators will in all cases use their training, experience and judgment to ensure that the hearing offers opportunities to claimants for healing and reconciliation. However, claimant counsel are cautioned that claims for AIL will unfold much differently than those where AIL is not claimed. In particular, the obligation on the part of adjudicators to apply the court causation standards in deciding AIL claims is such that a great deal of questioning is required in areas that are not as critical when the standard is “plausible link”. Of necessity, AIL hearings will be more time consuming. Adjudicators will have to delve in greater depth into questions of other potential causes / factors relating to a claimant’s lack of actual income and harms. In other words, before advising a claimant to check off “AIL” in the application, claimant counsel should carefully consider the availability of evidence to support an AIL claim, as well as the potential repercussions to the claimant in terms of:

- The nature and quality of a “causation” hearing, compared to a “plausible link” hearing;

- The possible negative impact of a causation hearing on opportunities for healing and reconciliation; and

- The additional health or emotional risks to the claimant associated with being subjected to the more rigorous questioning regarding causation and earnings history.

- Suggested Materials in Support of AIL Claim

- If after considering the above factors, claimants and their legal counsel choose to advance a claim for AIL, legal counsel are expected to play a significant role in ensuring that the materials and evidence necessary to establish such a claim are brought forward. The reasons for this are straightforward:

- As adjudicators are instructed to decide such claims “according to the same standards as a court would apply in like matters,” adjudicators expect counsel to provide materials and organize them in such a way as would be expected by the courts – this task is especially important as:

- There is no examination for discovery process available under the IAP;

- The IAP embodies an inquisitorial process, in which adjudicators are not entitled to investigate and locate evidence; and

- Adjudicators should not be expected to organize the evidence.

- The burden is on a claimant to establish a claim for AIL. Applying Practice Direction PD-1 (Schedule A), the adjudicator will make an assessment of credibility and determine whether there is a prima facie basis to support a claim within the complex track based on the claimant’s evidence. In other words, counsel should not expect or anticipate that if the evidence does not establish at least a prima facie claim of AIL by the end of the Claimant’s testimony, it can somehow be shored up by expert evidence or other documents at a later stage. If the case for AIL is not made out after the Claimant’s testimony, the case will revert immediately to the standard track, unless the claim is based on Other Wrongful Acts.

- As adjudicators are instructed to decide such claims “according to the same standards as a court would apply in like matters,” adjudicators expect counsel to provide materials and organize them in such a way as would be expected by the courts – this task is especially important as:

- Whether the AIL claim is for loss of employment, business, or traditional income, careful thought needs to go into which documents are “mandatory” and which documents are “available”, as those terms are discussed below. The two are not the same. In other words, mandatory documents necessary to establish a consequential loss of opportunity claim under IAP may not be adequate to fully support a claim for AIL.

- Mandatory documents;

The IAP does not specify exactly what documents are mandatory in AIL claims. , However, adjudicators will expect that all of the documents required to establish both Harms and Consequential Loss of Opportunity at levels 3 through 5 (pp. 28 and 29, IAP) are the minimum documents necessary to establish a prima facie AIL claim. - Available documents

Although “mandatory documents” refers to “Income Tax records (if not available, then EI and CPP records”), in claims for historical loss of actual income, income tax records from CRA may only be available for recent years. Therefore, such records would not necessarily even relate to the period of alleged loss or the years during which the earnings track record was being established.

Therefore, at a minimum, the following documents should be requested, covering the Claimant’s entire life between the commencement of work and retirement (or the present time if the Claimant is still working):

- Curriculum Vitae / Resume: A comprehensive summary of the claimant’s education and work history should be supplied.

- Education Records: The process for obtaining education records varies from one province or territory to another. Depending on the jurisdiction, education records may be kept by provincial or territorial departments of education, school boards or districts, or individual schools. Claimant counsel should request cumulative or permanent records, including academic, scholastic achievement and attendance records, for primary and secondary education. Post-secondary records are typically available directly from the institution the claimant attended.

- CPP records: The best data will be available by requesting a full employment history in letter form: Schedule B sample letter. HRSDC will provide a letter setting out the claimant’s employers, income and CPP contributions by year, dating back to 1967.

- Tax records from CRA: The best data will be available by requesting complete tax records as far back as they are available: Schedule C sample letter. If CRA cannot provide Income Tax records for the relevant periods, efforts should be made to attempt to locate T4s showing employment income, either from a claimant’s own records, from his or her former employer’s records, co-workers, or perhaps archival records;

- Employment records: It may be advisable to request the claimant’s personnel files from previous employers.

- Social assistance records.

- Claims for loss of actual traditional income: Counsel should give consideration to what types of data may be available to assist in evaluating the claim – these may include such data as land use, environmental impact and fisheries studies.

- Mandatory documents;

- Failure to supply appropriate documentary proof of all elements of the AIL claim may result in the claim not meeting the prima facie test, and being sent back to the standard track.

- Claimant counsel are expected to complete an AIL Data Worksheet: Schedule D, with such modifications as may be necessary, covering the basic elements of the AIL claim. This should be supplied to the Secretariat prior to the Pre-hearing Teleconference (Complex Track). This should make the hearing flow more smoothly and enable the parties to better consider whether admissions or settlement may be possible.

- In order for the adjudicator to properly retain and instruct a financial expert, Claimant Counsel and the Defendants’ representatives should bring to the hearing or supply beforehand:

- Proposals as to what type of financial expert may be most appropriate;

- Suggestions as to who the expert should be;

- A list of questions they propose that the adjudicator ask such expert;

- A list of legal issues that they submit arise from the facts of the case; and

- Court decisions in like matters that relate to the issues of causation and actual income loss that counsel submit are relevant to the issues to be decided, with relevant portions high-lighted.

- Due to the complexity of AIL issues, adjudicators will strongly encourage self-represented claimants to consult legal counsel. If self-represented claimants choose to proceed without counsel, adjudicators will give such directions as they consider necessary, to modify the above.

- If after considering the above factors, claimants and their legal counsel choose to advance a claim for AIL, legal counsel are expected to play a significant role in ensuring that the materials and evidence necessary to establish such a claim are brought forward. The reasons for this are straightforward:

Schedule A

Practice Direction PD-1

Re: Complex Track: Preliminary Case Assessments

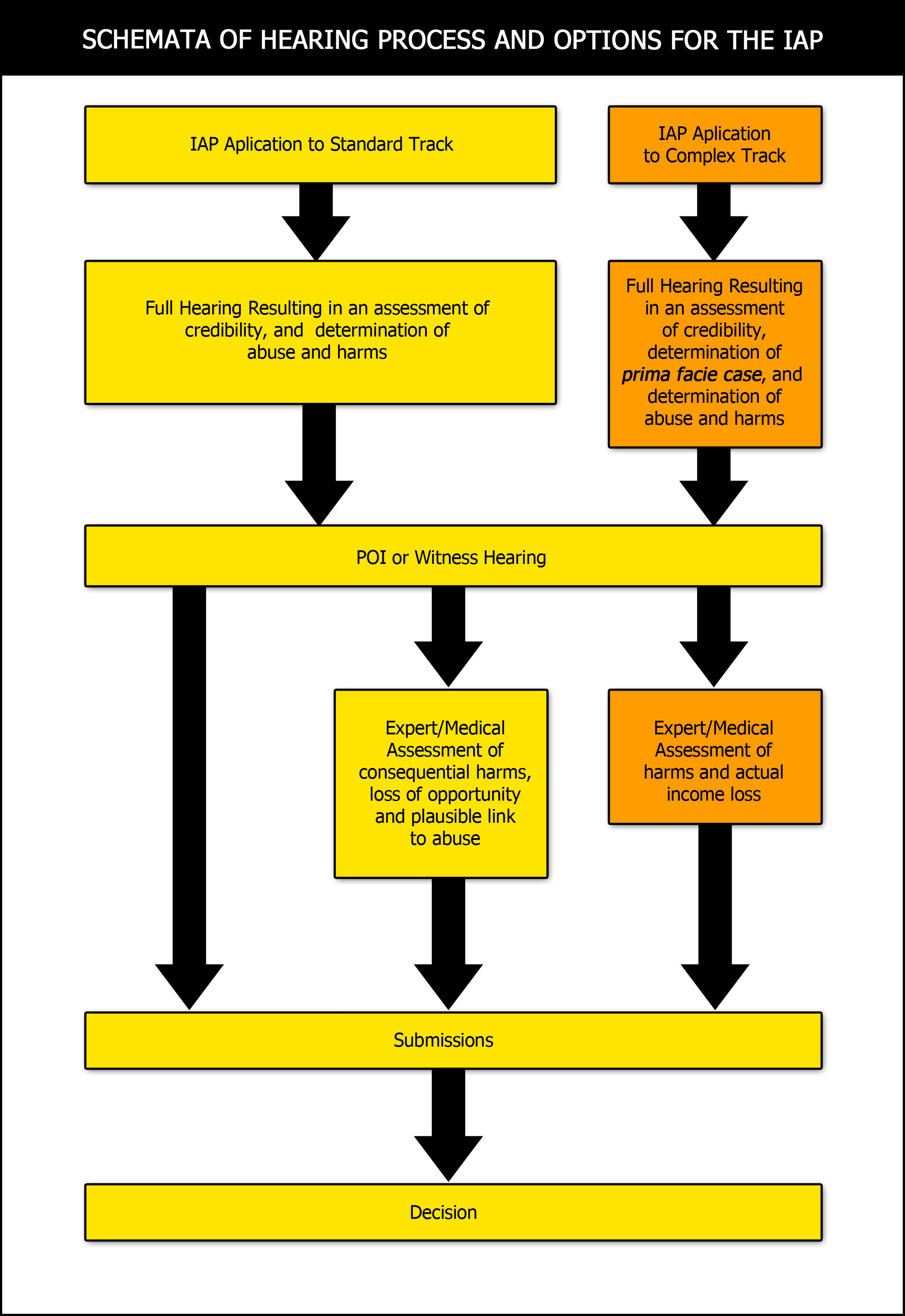

In the complex issues track, when a case is ready to proceed to hearing:

- The IAP Secretariat will arrange the initial hearing for the taking of all of the Claimant’s evidence. The Claimant will answer all questions put by the adjudicator. Based on the Claimant’s evidence, the adjudicator will make an assessment of credibility and determine whether there is a prima facie basis to support a claim within the complex track.

- If a prima facie basis to support a claim within the complex track is not made out, then the claim will continue (in the same hearing) under the standard track unless the only allegation in the claim is in the Other Wrongful Act category in which case the claim will not proceed.

- If a prima facie basis to support a claim within the complex track is made out, then the adjudicator shall arrange for expert assessments required by the standards set in the IAP. The IAP Secretariat will also make arrangements for hearing the evidence of any witness in relation to the claim or any alleged perpetrator.

- On the receipt of expert and/or medical evidence or at any point if such have been waived, the government and the Claimant may attempt to settle the claim having regard to the available evidence, the preliminary assessment of credibility, and all other evidence.

- If attempts to settle are not made, or if attempts are unsuccessful, then the claim will proceed to conclusion and decision, including recalling the claimant if appropriate circumstances exist.

- It is intended that this direction, or any interpretation of it, should not detract from any procedural or substantive rights of a claimant or other party that are provided in the IAP.

Commentary:

This proposed Practice Direction is intended to accomplish the following:

- Cases will flow smoothly through the entire IAP. Every case ready for hearing, whether in the standard or complex track, will first proceed with the claimant’s evidence. If it turns out that a complex issues track claim should have proceeded under the standard track, it can move in that direction immediately after the claimant’s evidence without the need to recall the claimant or have another hearing.

- In many cases the parties will only have to get together once, for the claimant’s evidence, rather than for a preliminary assessment hearing and a final hearing later. This will avoid unnecessary delays due to scheduling of two hearings instead of one. Benefits of this include less time to the conclusion of a case, lower cost hearings, and less potential to re-victimize the claimant.

- The process avoids the unnecessary delays that might result from new or more detailed disclosures of abuses or harms late in the process at the second hearing.

- The process allows for witness and POI testimony to proceed without having to wait for the second hearing with the claimant, which second hearing occurs later in the process under the current b.viii.

- Adjudicators will have detailed evidence with which to assess the claim and on which to instruct experts. Preparation of directions to experts will take less time and will therefore be less costly. Experts will make their assessments based on detailed evidence. Expert assessments will likely take less time because the expert will already have detailed information from the transcript. Directions to the experts will, therefore, be based on concrete evidence already heard rather than possibilities.

- This process results in a proper record of all proceedings, thereby meeting the procedural fairness requirements in administrative law. The proposed process will result in all claimants’ having a right of review under the IAP.

- The hearing process will be completely transparent and the risk of inconsistencies will be greatly reduced.

- In addition, a pre-hearing management conference (normally by conference call) is contemplated to allow the parties and the adjudicator to assess the readiness of the claim to proceed in the complex track.

Overall, this amendment will maintain the spirit and intent of the complex issues track provisions while at the same time creating a more streamlined, more sensitive, timelier, and less costly process.

Attached as Appendix “A” is a graphic illustration of the proposed process.

Approved by IAP Oversight Committee: January 15, 2008

Approved by National Administration Committee: January 17, 2008

Schedule A

.

.

image: SCHEMATA OF HEARING PROCESS AND OPTIONS FOR THE IAP

Click here for a text version.

Schedule B

Sample letter to HRSDC, requesting comprehensive historical CPP data

25 March, 2008

Human Resources Skills Development Canada

Income Security Programs

Canada Pension Plan

P.O. Box 9750, Postal Station “T”

Ottawa, ON K1G 4A6

Attention: Joanne Plouffe-Dubé

Dear Ms. Plouffe-Dubé:

Re: «ClientLastName», «ClientFirstName» «ClientMiddleName»

«ClientAKA» SIN:

«ClientSIN» «ClientSSN»

DOB: «ClientDOB»

I act for «ClientFirstName» «ClientLastName» with respect to a personal injury matter and, accordingly, I am enclosing an Authorization to Communicate Information form signed by «ClientFirstName» «ClientLastName».

Please provide me with a complete Canada Pension Plan employment history in letter form regarding «ClientSalutation» «ClientLastName» for the years 1967 to present.

If you have any questions regarding this request or need more information, please contact my assistant, «ParalegalName», at (___) _______.

Yours sincerely,

Enclosure

Sample letter to HRSDC, requesting Authorization to release information

TO: Human Resources Development Canada

Access to Information & Privacy

140 Promenade du Portage

Phase IV, Level 1, Mail stop 112, Gatineau, QC K1A 0J9

RE: «ClientFirstName» «ClientMiddleName» «ClientLastName», aka «ClientAKA»

SIN: «ClientSIN»«ClientSSN»

I, «ClientFirstName» «ClientMiddleName» «ClientLastName», HEREBY authorize and consent to the release of a complete Canada Pension Plan Statement of Contributions and Employment History including earnings information for each employer in the form of a letter relating to «ClientFirstName» «ClientMiddleName» «ClientLastName», presently residing at «ClientCity», «ClientProv», for the years XXXX to present to «ResponsibleLawyer», barrister and solicitor,

I CONSENT to the use of this information by the authorized recipient only, for the purpose of an Indian Residential School claim.

I am the contributor and understand the nature and effect of this authorization. DATED:

«ClientFirstName» «ClientLastName»

RESTRICTIONS

The regulations provide that the information cannot be communicated:

- If the authorization is signed more than one year before the date it is received;

- If more than one request for information concerning the same contribution or beneficiary is made in the same year and is to be communicated to the same person or authority;

- If I cancel this authorization in writing.

THIS FORM CAN NOT BE FAXED OR SENT BY E-MAIL

Schedule C

Sample letter to CRA, requesting comprehensive historical income tax data

25 March, 2008

The Director

Surrey Taxation Centre

9755 King George Highway

Surrey, BC

V3T 5E1

Dear Sir or Madam:

Re: «ClientLastName», «ClientFirstName» «ClientMiddleName»«ClientAKA»

SIN: «ClientSIN» «ClientSSN»

DOB: «ClientDOB»

Please find enclosed a release form signed by «ClientFirstName» «ClientLastName» authorizing the release to this office, for civil litigation purposes, of his complete taxation records, as far back as they are available. This request does go beyond the time when your records were placed in the present computer system.

I agree to pay your reasonable fees for searching and copying.

Yours sincerely,

Enclosure